Few things feel more frustrating than checking your credit score and realizing it’s gone down. Maybe you were expecting to see progress, or at least stability, and instead you see a dip that leaves you confused and worried.

First things first: don’t panic. A credit score drop doesn’t automatically mean disaster, and in many cases, it’s temporary and fixable. The key is to figure out why it happened and then take steps to get things moving back in the right direction.

Let’s break down some of the most common reasons credit scores drop – and what you can do about it.

Common Reasons Credit Scores Drop

1. Late or Missed Payments

Your payment history makes up the biggest chunk of your credit score. Even one missed payment can have a noticeable impact. The later the payment (30, 60, 90 days), the bigger the hit.

2. High Credit Utilization

Using too much of your available credit – even if you’re paying on time – can drag your score down. Experts recommend keeping your utilization below 30%, but the lower, the better.

3. New Credit Applications

Every time you apply for a new credit card, loan, or line of credit, a “hard inquiry” appears on your report. A single inquiry won’t hurt much, but too many in a short period of time can cause your score to dip.

4. Closing Old Accounts

You might think closing an old credit card you don’t use is a good idea, but it can shorten your credit history and reduce your overall available credit – both of which can lower your score.

5. New Negative Items

Collections, charge-offs, or bankruptcies are bigger blows to your credit and can cause sharp drops. These need special attention to resolve.

6. Credit Report Errors

Believe it or not, mistakes happen all the time. Accounts reported twice, payments marked late when they weren’t, or even someone else’s debt showing up on your file can unfairly bring your score down.

How to Identify What Happened

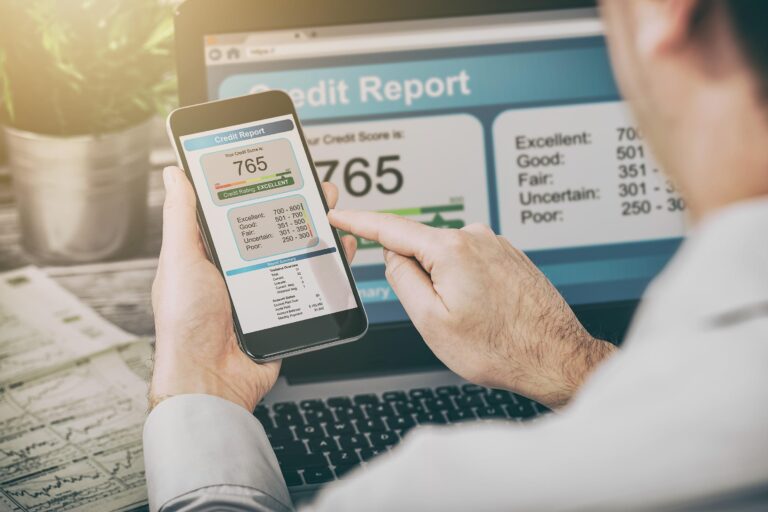

Before you can fix the problem, you have to figure out what caused it. Start by pulling your credit reports from all three major bureaus: Experian, Equifax, and TransUnion.

Look closely at:

- New accounts or inquiries

- Payment history updates

- Collection accounts or judgments

- Any items you don’t recognize

If you’re monitoring your credit regularly, you might even catch changes in real time. That makes it easier to pinpoint the exact cause of the drop.

What to Do About It

Now that you know why your score went down, here’s what to do next:

- If it’s late or missed payments: Get current as soon as possible. Set up autopay or reminders to avoid missing future due dates. Over time, consistent on-time payments will outweigh one mistake.

- If it’s high utilization: Focus on paying balances down. You can also request a credit limit increase (without increasing spending) to instantly lower your utilization ratio.

- If it’s hard inquiries: Space out applications for credit, and only apply when you really need to. Inquiries age off over time, so patience is key here.

- If it’s a closed account: Don’t worry – the impact lessens over time. Focus on keeping your other accounts in good standing.

- If it’s a new negative item: Contact the creditor or collection agency to explore options for resolution. Sometimes you can negotiate payments or even removals.

- If it’s an error: File a dispute with the credit bureau. Under federal law, they must investigate within 30–45 days.

The important thing is to act quickly. The sooner you address the cause, the sooner your score can start recovering.

How to Prevent Future Drops

A dip in your score can be a wake-up call to tighten up your credit habits. Here are some ways to stay ahead:

- Set up autopay or calendar reminders so payments are never late.

- Keep balances low – ideally below 30% of your credit limit.

- Avoid applying for too much new credit at once.

- Check your credit reports at least once a year for accuracy.

- Build a financial cushion so emergencies don’t lead to missed payments.

Consistency is your best friend when it comes to credit. The longer you show good habits, the more resilient your score becomes.

Where Kaydem Can Help

Here’s the thing: sometimes, you can do everything right and still feel stuck. Errors on your report, old collections, or complicated situations aren’t always easy to untangle on your own.

That’s where Kaydem Credit Help comes in. Our team has helped thousands of people identify the exact reasons their scores dropped – and take the right steps to fix them. Whether it’s disputing errors, negotiating with creditors, or building a personalized strategy, we know how to turn things around.

Many of our clients start to see real improvements in just a few months because we don’t just guess – we target the exact issues holding them back.

If your score has dropped and you’re not sure what to do next, don’t waste another day worrying. Sign up with Kaydem Credit Help today and let us help you build the future you’ve been dreaming of.

Final Thoughts

A sudden dip in your credit score can feel discouraging, but it’s rarely the end of the story. In most cases, there’s a clear reason behind the drop – and a clear path to fixing it.

The key is to act quickly, stay consistent, and get the right support when you need it. Your credit story isn’t defined by one setback. With the right steps, you can bounce back stronger than ever.